March 30, 2026

Via www.regulations.gov

Docket No. IRS-2026-0166-0001

Internal Revenue Service

Attn: CC:PA:LPD:PR (Notice 2026-15), Room 5203

P.O. Box 7604, Ben Franklin Station

Washington, DC 20044

Re: Notice 2026-15, Guidance to Apply Interim Safe Harbors for Purposes of Determining a Taxpayer’s Material Assistance from a Prohibited Foreign Entity; Other Prohibited Foreign Entity Guidance

Responsible Battery Coalition (RBC) Background. The RBC is a coalition of companies, academics, and organizations committed to the responsible management of the batteries of today and tomorrow. Founded in 2017, The RBC was created to advance the responsible production, transport, sale, use, reuse, recycling, and resource recovery of transportation, industrial, and stationary batteries, as well as other energy storage devices. RBC’s diverse membership represents the entire battery lifecycle and includes the world’s leading battery manufacturers, recyclers, automotive fleet management, automotive retail, and original equipment manufacturers. For more information: https://www.responsiblebatterycoalition.org/

General Policy Rationale. RBC submits these comments to emphasize that batteries are a vital driver of the American economy and to underscore the importance of the 45X Advanced Manufacturing Production Tax Credit for the domestic battery manufacturing sector. We appreciate the Administration’s efforts to boost manufacturing in America, create high-paying American jobs, secure critical mineral supply chains to protect the industry from foreign market manipulation, and promote broader national and energy security goals. The 45X Tax Credit helps advance these aims, and we encourage the Treasury to formulate a proposed regulation that maximizes benefits for American companies and consumers from the tax credit, while also preventing American taxpayer dollars from supporting foreign companies, especially those linked to prohibited or foreign-influenced entities. To support this, we offer the following comments to clarify and reinforce elements in the interim guidance included in IRS Notice 2026-15.

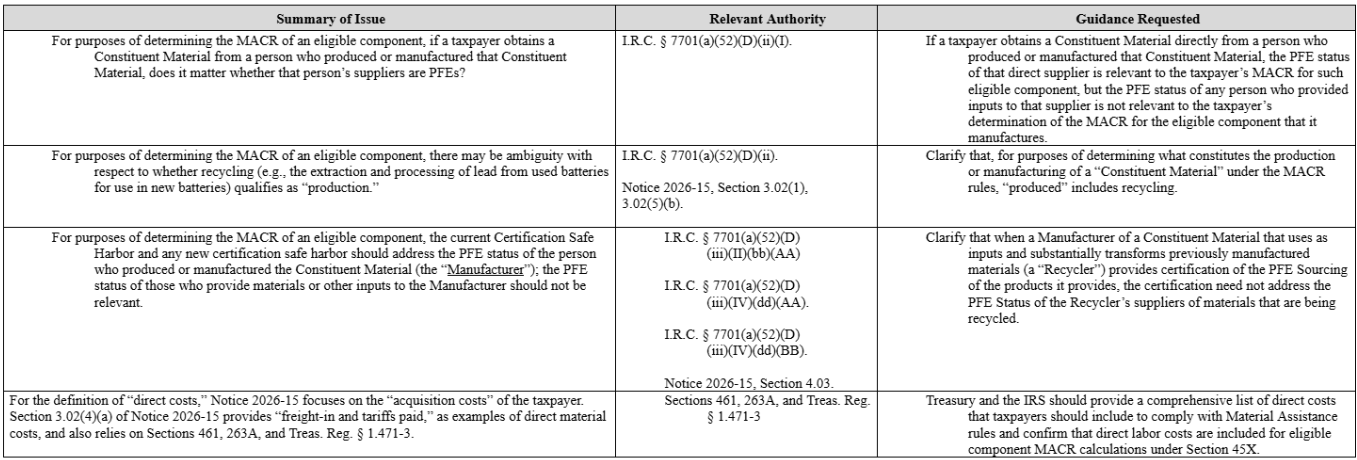

I. Summary of Key Recommendations.

II. PFE Status of Persons Who Supply a Manufacturer/Producer of a Constituent Material.

a. Context.

I.R.C. § 7701(a)(52)(D)(ii)(I) provides that in determining a taxpayer’s MACR with respect to an eligible component, one amount that matters is “the total direct material costs that are paid or incurred ... by the taxpayer for production of such eligible component that are mined, produced, or manufactured by a prohibited foreign entity.”

Notice 2026-15, Section 3.02(5)(a), describes this amount as the Direct Material Costs attributable to each Constituent Material that is PFE Sourced.

Notice 2026-15, Section 3.02(5)(b) provides that a Constituent Material is PFE Sourced if it is supplied to the taxpayer by a person that is a PFE. That section also provides that if the supplier is a mere reseller, then the PFE status of the person that mined, produced, or manufactured the Constituent Material is relevant.

b. Guidance Requested.

We strongly support the approach adopted in Notice 2026-15. Under this approach, the PFE Status of the person who mined, produced, or manufactured a Constituent Material may be relevant, but it does not matter whether that person’s suppliers were PFEs. For example, if a taxpayer purchases a Constituent Material from the person who manufactured the Constituent Material (the “Manufacturer”), what matters is whether the Manufacturer is a PFE, not whether any of the Manufacturer’s suppliers are PFEs.

This approach makes the MACR calculation administrable, and it promotes the statutory goal of encouraging production and manufacturing by entities that are not PFEs.

We request that any future guidance adopt this same approach.

III. Recycled Constituent Materials and the Eligible Component MACR.

a. Context.

Battery recycling is a complicated and technical process that substantially transforms the inputs (used batteries) to extract and process lead so that it is suitable for use in newly manufactured batteries.

b. Guidance Requested.

Treasury should clarify that, for purposes of determining what constitutes “production” or “manufacturing” of a Constituent Material, “produced” or “manufactured” includes recycling.

In particular, in the context of recycled batteries, Treasury should confirm that a recycler that extracts and processes lead from used batteries so that it may be used in the production of new batteries (a “Recycler”) is “producing” lead and hence is not a “mere reseller” under Notice 2026-15, Section 3.02(5)(b). The PFE status of those who provide the Recycler with the materials it uses to recycle batteries (e.g., the supplier of used batteries) does not affect the extent to which the lead is treated as being PFE Sourced.

c. Support.

Congress and Treasury have repeatedly taken the position recycling qualifies as a manufacturing or production activity that generates something new and is not merely “reselling.”

Section 45X guidance states that the regulations explicitly provide that the “term produced by the taxpayer . . . includes both primary and secondary production. Primary production involves producing an eligible component using non-recycled materials while secondary production involves producing an eligible component using recycled materials.” Treas. Reg. § 1.45X-1(c)(1).

Even setting aside the explicit inclusion of recycling processes, the general definition would also include these processes in that the “term produced by the taxpayer means a process conducted by the taxpayer that substantially transforms constituent elements, materials, or subcomponents into a complete and distinct eligible component that is functionally different from that which would result from minor assembly or superficial modification of the elements, materials, or subcomponents.” Id.

Domestic Content Notice 2023-38 defines “manufacturing process” as “the application of processes to alter the form or function of materials or of elements of a product in a manner adding value and transforming those materials or elements so that they represent a new item functionally different from that which would result from mere assembly of the elements or materials.” Notice 2023-38, Section 3.02(e).

This interpretation is supported by policy goals, which center on incentivizing domestic manufacturing and production, including domestic recycling. The Recycler is the entity that “produces” or “manufactures” the Constituent Material. Any transactions that occurred before the recycling are not relevant to determining the incentives provided to recyclers, producers, and manufacturers today.

IV. Certification Safe Harbor for Recycled Constituent Materials.

a. Context.

To simplify a taxpayer’s burden of proving the extent to which its Constituent Materials are PFE Sourced, the statute and the Notice provide a safe harbor under which the taxpayer is treated as satisfying its burden of proving the extent to which its Constituent Materials are PFE Sourced by obtaining certifications about the PFE status. This safe harbor is available until the government provides safe harbor tables pursuant to I.R.C. § 7701(a)(52)(D)(iii)(I).

For a taxpayer that produces or manufactures an eligible component and seeks a Section 45X tax credit, the certification may be provided by a supplier of a “constituent element, material, or subcomponent [i.e., a Constituent Material] of an eligible component ... (BB) that such product or component was not produced or manufactured by a prohibited foreign entity” (the “General Certification Requirement”) I.R.C. § 7701(a)(52)(D)(iii)(II)(bb).

The statute also requires that one of three conditions be satisfied. The two that may be relevant in the context of eligible components and the Section 45X tax credit are that the certificate states either:

(AA) “that such property [the Constituent Material] was not produced or manufactured by a prohibited foreign entity and that the supplier does not know (or have reason to know) that any prior supplier in the chain of production of that property is a prohibited foreign entity” (the “AA Rule”); or

(BB) “the total direct material costs for each component, constituent element, material, or subcomponent that were not produced or manufactured by a prohibited foreign entity” (the “BB Rule”).

I.R.C. § 7701(a)(52)(D)(iii)(II)(bb)

b. Guidance Requested.

Clarify that under the current Certification Safe Harbor, when a taxpayer acquires a Constituent Material from the person who produced or manufactured that Constituent Material (i.e., the Manufacturer), the certification provided by the Manufacturer need only address the PFE Status of the Manufacturer; the taxpayer does not need to obtain certification of the PFE Status of any of the Manufacturer’s suppliers.

Provide a permanent safe harbor that adopts the same approach, so that a taxpayer may rely on a certification of the Manufacturer’s PFE Status, without regard to the PFE Status of those who supplied materials or other inputs to the Manufacturer.

In the context of battery recycling, confirm that a Recycler may provide a battery manufacturer with a certificate that addresses the Recycler’s PFE Status, and that the taxpayer does not need any certification or information about the PFE Status of those who provided the Recycler with its previously manufactured inputs (i.e. used batteries) that are being recycled.

c. Support / Analysis.

A certification safe harbor should be a procedural rule by which a taxpayer can establish that it has complied with statutory requirements; it should not change the rules regarding the extent to which a Constituent Material is PFE Sourced.

The General Certification Requirement is consistent with this approach, for it focuses on the person who produced or manufactured the Constituent Material (the Manufacturer), not those who produce or supplied the inputs for the Manufacturer.

In addition, under the temporary certification rule, the certification must satisfy either the AA Rule or the BB Rule. Both of these rules are consistent with certification being limited to the PFE status of the Manufacturer, and not addressing the PFE status of those who produce or supply the inputs for the Manufacturer, in the case of a Recycler.

The AA Rule has two parts.

The supplier must provide a certificate that states that the Constituent Material was not produced or manufactured by a PFE. This is consistent with the General Certification Requirement and its focus on who produced or manufactured the Constituent Material (the Manufacturer), not those who supplied the Manufacturer.

The supplier must also certify that it does not know (or have reason to know) that any “prior supplier in the chain of production” of that property is a PFE.

As an initial matter, this requirement should be interpreted consistently with the general principles of determining PFE Sourcing of a Constituent Material and the General Certification Requirement: what matters is the PFE status of the Manufacturer (i.e., the person who produced or manufactured the Constituent Material). In the case of recycled batteries, only the PFE status of the Recycler should be considered relevant.

However, even in the alternative (i.e., if Treasury issues rules requiring “look through” to Manufacturers’ upstream suppliers for the Certification Safe Harbor), in the case of Recyclers, certifications should not be required to address the PFE Status of the Recycler’s suppliers of materials that are being recycled. This is because the source of previously manufactured used batteries transformed by such Recycler into Constituent Materials should not be considered to be in the “chain of production” of the Constituent Materials by such Recycler. The chain of production for a spent battery delivered by a reseller to a Recycler should begin with the Recycler and continue through until the Constituent Material is supplied to the taxpayer. Any prior “chain of production”—for instance, when the battery was first made, prior to its use—should not bear on the MACR calculation for the recycled battery.

This serves policy goals of incentivizing recycling and domestic recycling industries. In addition, this provides an administrable rule, as it is difficult for a battery manufacturer to trace the prior chain of production of a spent battery that was an input to their purchased recycled lead.

The BB Rule is an alternative to the AA Rule. The BB Rule clearly focuses on the PFE Status of the person who produced or manufactured the Constituent Material, not the PFE Status of any of its suppliers.

Thank you for your attention to this matter and for considering RBC’s perspective on this important issue. RBC welcomes the opportunity to engage with Treasury as it develops a proposed regulation that builds on this interim guidance. If you have questions, please do not hesitate to contact: Steve Christensen, Executive Director, Responsible Battery Coalition, steve@responsiblebattery.org

Respectfully submitted,

Steve Christensen

Executive Director

Responsible Battery Coalition

1455 Pennsylvania Ave., NW, Suite 400

Washington, DC, 20004